In today’s fast-paced financial environment, flexibility is key. Whether you’re managing personal finances or running a business, having access to funds when needed can be a game-changer. One of the most versatile borrowing options available is the line of credit loan. But what exactly is it, how does it work, and when should you consider using one?

This comprehensive guide explains what a line of credit loan is, how it differs from traditional loans, the types available, and how to use it wisely.

Definition: What Is a Line of Credit Loan?

A line of credit (LOC) loan is a flexible borrowing option that allows individuals or businesses to access funds up to a pre-approved limit, withdraw as needed, and pay interest only on the amount used—not the total limit.

Think of it as a credit card without the card: you can draw funds when necessary, repay them, and borrow again within the set limit, without reapplying.

How Does a Line of Credit Work?

Key Features:

- Pre-approved credit limit (e.g., $5,000 – $100,000+)

- Flexible withdrawals up to the credit limit

- Interest charged only on borrowed amount

- Revolving access—funds become available again after repayment

- Can be secured or unsecured

With a line of credit, borrowers have the freedom to manage short-term cash needs, emergencies, or irregular expenses without taking on a fixed-term loan.

Types of Line of Credit Loans

1. Personal Line of Credit

A personal line of credit is an unsecured loan available to individuals with good credit and income.

Use Cases:

- Emergency expenses

- Home repairs

- Debt consolidation

- Large purchases

Pros:

- No collateral required

- Flexible use of funds

- Lower interest than credit cards

Cons:

- Requires good credit

- Interest rates may fluctuate

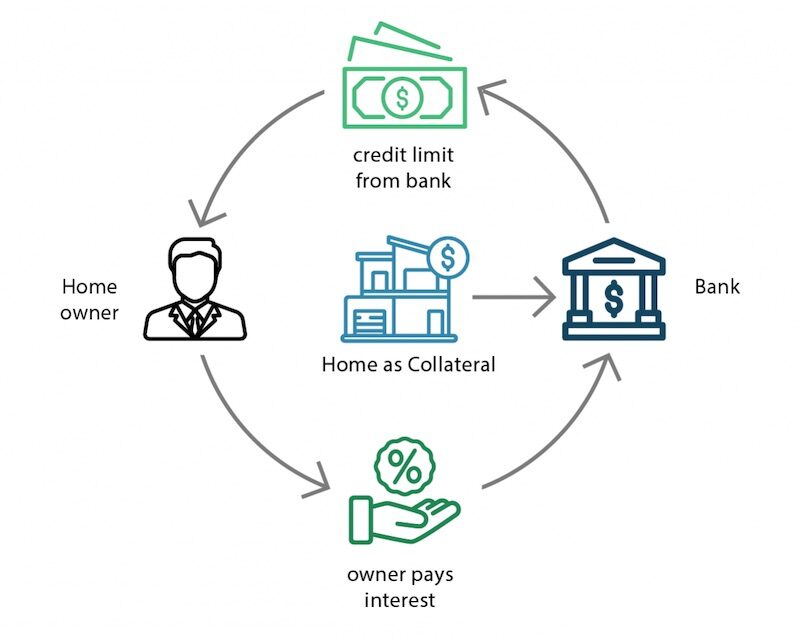

2. Home Equity Line of Credit (HELOC)

A HELOC is a secured line of credit using your home as collateral. The credit limit is based on the equity in your home.

Use Cases:

- Home renovations

- Education costs

- Medical bills

Pros:

- Larger credit limits

- Lower interest rates

- Tax-deductible interest (in some cases)

Cons:

- Your home is at risk if you default

- May have draw and repayment periods

3. Business Line of Credit

Designed for small to medium-sized businesses to manage operational costs, inventory purchases, or seasonal cash flow gaps.

Use Cases:

- Payroll

- Marketing expenses

- Equipment purchases

- Covering delayed receivables

Pros:

- Boosts working capital

- Only pay interest on what you use

- Renewable after repayment

Cons:

- Requires business financial documentation

- May include maintenance fees or draw fees

Line of Credit vs. Traditional Loan

| Feature | Line of Credit | Traditional Loan |

|---|---|---|

| Borrowing Amount | Withdraw as needed | Lump sum upfront |

| Interest Payments | Only on what is used | On entire loan amount |

| Flexibility | High | Low |

| Repayment Terms | Variable | Fixed |

| Reusability | Yes | No |

| Application Process | May be longer | Often faster |

A line of credit is best for ongoing or unpredictable expenses, while a traditional loan suits one-time, large purchases.

How to Get a Line of Credit

Step 1: Review Your Credit Profile

Lenders assess:

- Credit score

- Debt-to-income ratio

- Income stability

- Employment history

Step 2: Determine the Type of Line of Credit

Decide whether you need:

- A personal LOC for flexible personal use

- A HELOC for leveraging home equity

- A business LOC to manage cash flow

Step 3: Compare Lenders

Shop around to compare:

- Interest rates

- Credit limits

- Fees (annual, maintenance, draw)

- Repayment terms

Step 4: Submit an Application

You’ll typically need:

- Proof of identity

- Proof of income (pay stubs, tax returns)

- Credit history

- Bank statements

For HELOCs or business LOCs, expect additional documentation.

Step 5: Access Funds

Once approved, you’ll receive access to your line of credit through:

- Online transfers

- Checks

- Debit cards (in some cases)

You can then draw funds at your discretion.

Repayment and Interest on a Line of Credit

Most LOCs require monthly payments based on the interest accrued and sometimes a portion of the principal. Repayment models may vary:

- Interest-only payments during the draw period

- Principal + interest after the draw period ends

Interest rates may be fixed or variable, depending on the lender and creditworthiness.

When Should You Use a Line of Credit?

A line of credit can be a lifesaver or a smart cash management tool in the following scenarios:

- Emergency medical expenses

- Home improvement projects

- Bridging temporary income gaps

- Covering seasonal business expenses

- Avoiding high-interest credit card debt

It should NOT be used for non-essential spending, or if you lack a clear repayment plan.

Advantages of a Line of Credit

✅ Flexibility: Draw only what you need, when you need it

✅ Revolving Access: Funds replenish after repayment

✅ Lower Cost vs. Credit Cards: Especially for good-credit borrowers

✅ Improves Cash Flow: Ideal for unexpected expenses

✅ Builds Credit: On-time payments help your credit score

Potential Drawbacks

❌ Variable Interest Rates: May increase unexpectedly

❌ Temptation to Overspend: Easy access can lead to debt

❌ Fees: Some lenders charge maintenance, withdrawal, or inactivity fees

❌ Credit Requirements: Approval is tougher with bad credit

❌ Risk to Collateral: For secured lines like HELOCs

Tips for Managing a Line of Credit Responsibly

- Only borrow what you need

- Track your spending

- Pay more than the minimum to reduce interest costs

- Avoid carrying balances long term

- Review statements regularly

- Maintain good credit habits

Using a line of credit wisely can be an asset. Mismanaging it can lead to spiraling debt.

Conclusion

A line of credit loan is one of the most versatile financial tools available to both individuals and businesses. It offers flexible access to funds, lower interest rates than many alternatives, and the ability to respond quickly to financial needs.

Whether you’re looking to finance home repairs, manage business operations, or cover emergency costs, a line of credit can be the perfect solution—as long as it’s used responsibly.